With an earnings event creating huge volatility, it seems logical to short a post-earnings play as it becomes “overextended”.

I’ve done a LOT of backtesting around this theory, and have not been able to materialize any hint of a profitable strategy.

Shorting momentum stocks with a strong catalyst like earnings can be dangerous because they can run for weeks.

Here are a few recent examples:

These charts remind me of the post earnings announcement drift strategy I wrote about a few years ago.

My buddy @adamtrades brought an interesting chart to my attention that made me consider a different type of earnings reversal pattern.

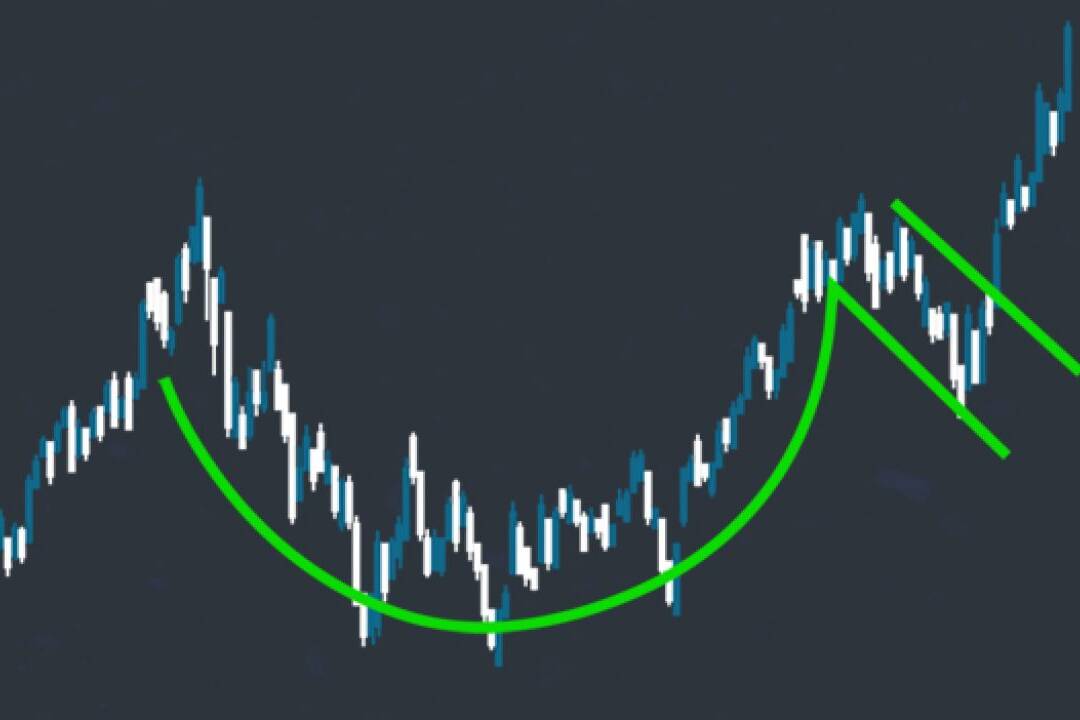

$JILL had a massive gap down on earnings day, closing -53% from the previous close. The selloff continued for a few days but then started to curl back up. This reversal from the low produced almost 37% returns over the following six days.

A quick scan revealed several other “earnings loser” reversals, and this was only looking at stocks that closed -20% or more on earnings day. I’m sure there are a lot more if you expand the search to include -5% or -10% or change ED % Chg. I also like to use ED % Chg from Open as a filter to get stocks with big earnings day candles.

Here are a few charts I picked out from that scan:

Related Posts

Beginner Stock Trading Tactics for Post-Earnings Momentum

Earnings season is an exciting time for stock traders, as it can lead to…

Buying Earnings Winners in Structural Bases: The Cup-with-Handle Approach

Successful stock trading often involves identifying patterns that signal…

Demystifying Earnings Events: A Beginner’s Guide for Entry-Level Traders

Earnings events are significant market occurrences that can greatly impact a…